- Introduction

- Age Considerations Before Investing

- Decision About Diversification

- How Much You Need

- How Much Should I Invest?

- Benefits of a 401(k)

- Can You Lose Money in 401(k)?

- Automating Your 401(k) Investments

- Auto-Escalation

- Target Date Funds

- Stay With Your Old Plan

- Move Your Savings

- Cash Out Your Savings

- How Much You Should Have Saved For Retirement

- Conclusion

Introduction

Contemporary society, more than ever before, requires people to have a plan on how they are going to lead their lives when they are out of the workforce. A 401(k) plan is integral to many people’s retirement saving strategy since the plans come with tax incentives, not to mention that the employer can match them. However, effective 401(k) investment management is not simple; it is always rich in decision-making issues. This guide is intended to give a wealth of information on how to get the most from your 401(k) by understanding and planning your investments well.

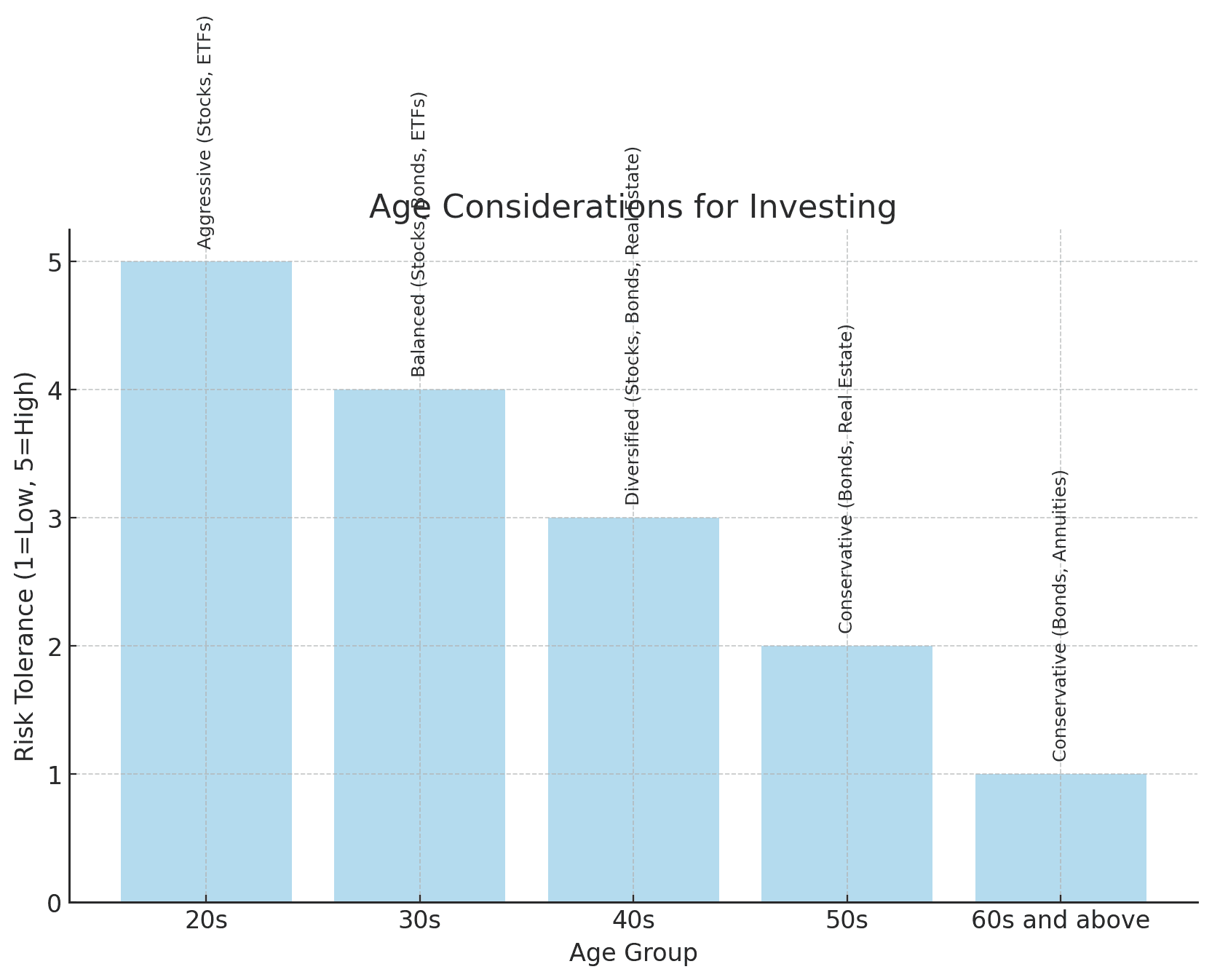

Age Considerations Before Investing

One aspect that will act as a guide to an investor in the 401(k) plan is their age. Younger persons have more years to live and can wait for a long time to have their money grow due to their ability to absorb risk from volatile growth-oriented instruments such as stocks. When you get closer to retirement, it becomes less wise among rational investors to start investing conservatively so that their accumulated wealth does not reduce by getting involved in the operation of the stock market.

Age is a key principle that largely determines the peculiarities of investing in a 401(k) plan and risk diversification. This means that how you invest depends on your life cycle stage: growth-oriented younger men can afford to be more aggressive than more conservative older women.

For the generation from young adulthood, the investment horizon is extended to several years and, in most cases, over several decades. This period also gives the younger generation investor a chance to earn compounding returns whereby increments are earned on both initial investment and the earned interests. As a result, young persons can lock in a higher aggregate risk onto their 401(k) portfolios than recommended by the efficient frontier by loading their portfolios with stocks. Subsequently, stock returns have been higher than other investments, such as bonds or cash investments, although stock risk is higher. Young investors’ main strength is their ability to wait out the market to come out on top, no matter the market’s direction.

Decision About Diversification

Thus, diversification is important for utilizing your 401(k) investments. It entails distributing the investment dollars to cover different forms of investments, industries, and geographical areas to moderate risk and increase returns. Learning how to save for the 401(k) and invest it diversely for the long haul is important for every person.

However, diversifying 401(k) is one of any investment portfolio’s basic objectives or goals. Stocks, bonds, cash, and fixed-income instruments are different types of security and thus function differently in the market. In this way, if any asset classes are in the red, it will not be possible to see a massive result because you invested in other promising classes. For instance, if the shares have underperformed for some reason, the bonds might have either held steady or posted better results, thus lessening the impact on the portfolio. This balance is important in creating a situation that can be sustained over the long term regarding business performance.

Since there are several options in the disposal of investing in their 401(K), it is necessary to determine the risk and return each class of assets will bring. This is why the return rate associated with stocks is higher than that of bonds but is also riskier. While stocks fluctuate, bonds are more stable, but their returns tend to be lower most of the time. For a diversified portfolio, such ultimate assets could combine these classes depending on the investor’s risk tolerance and investment time frame. Therefore, if the investors are young and they have many years until their retirement, then stocks as an investment option could be suitable for them. On the other hand, investors close to retirement age need to invest more in bonds since they come with less risk.

How Much You Need

Assessing the amount one needs to have in the 401(k) by retirement is an important factor to plan for. Knowledge of this figure is useful in planning the savings strategy and other actions related to the distribution of 401(k) investments. The sum one needs for retirement differs due to several factors, such as the preferred lifestyle, health care expenses, etc.

Thus, according to financial planners’ criteria, people should target receiving about 70-80% of their income from their pension before retirement. For instance, if your yearly income is $100,000, your retirement income is $70,000-$80,000 per year. This has been a handy rule of thumb for developing an initial estimate of retirement planning.

One should estimate annual living costs to set a more personalized amount to save for retirement. These include food, shelter, transport, medical services, and other wants such as holidays and entertainment. A particular parameter that one should also consider is the effects of inflation, as this reduces the purchasing power par value. Budgeting with an annual inflation rate of 2 to 3% is normal.

How Much Should I Invest?

Determining how much of your earnings you should put into your 401(k) is one way of adequately preparing for retirement. Your input decides how your retirement savings will grow, and a small input into your 401(k)-investment decision can go a long way in improving your returns while minimizing risks.

One piece of advice that most financial specialists give is that to save for retirement, one should be prepared to put at least 15 percent of their gross income towards this effort. This figure also includes any contribution made by the employer’s Insurance. For instance, if the employer’s contribution to the 401(k)-plan scheme is equal to 5% of the employee’s salary, then the employee must put 10% of their salary towards the scheme as per the 15% target. Employer matches on contributions can be said to be free money, which has to be used to the maximum for one to have the best retirement plans.

Benefits of a 401(k)

401(k) plan includes several advantages, which is why it is a key concern for many employees and their retirement planning. Knowing these advantages can make one realize why contributing to such a plan is vital and, therefore, the ability to decide on the distribution of the 401(k) investment.

Consequently, the 401(k) plan offers numerous advantages, the most important being the taxation regime. Deductions to a conventional 401(k) are made before tax. Therefore, the money allocated will be less than the taxes for the year. Such effects can result in massive tax savings, particularly for individuals who fall under the higher tax bands. Filed under 401(k) plans, the money then accrues tax-sheltered, whereby one does not receive taxation on any earnings on the invested funds until they retire. This allows your investments to grow in capital and compound without yearly taxes.

Trading one tax benefit for another, a Roth 401(k) differs in tax advantage. It is contributed from after-tax money; thus, it does not affect your current gross income. However, the main advantage is that all withdrawals in retirement are not subject to any taxes if one has met the basic requirements. This can be of particular value, especially if one believes they will end up in a higher tax bracket in their retirement than they currently are. Knowing how to divide your 401(k) contributions between the regular and the Roth ones will help you prevent unnecessary taxes at the current and future stages.

Another feature of 401(k) plans that encourages participation is the employer’s matching contributions. Some employers even contribute to the extent of matching some part of your investment, offering you more cash to fund your retirement annuities, all for free. For example, an employer can match the dollar up to 6% of your salary. For instance, an employer could contribute 50 cents on the dollar up to 6% of your salary. Maximizing this match is easily one of the best things you can do for your 401(k) investment because you are sure that your money will grow immediately if you invest it.

Can You Lose Money in 401(k)?

Most people need to realize that while a 401(k) could be a great way to save for retirement, it carries some risks like any other investment. It is possible to lose money when you invest in a 401(K), and for this reason, the question that everyone can potentially ask is, “Can you lose money in the 401(K)? Yes, you can lose money in a 401k, but you should know how certain choices can lead to your account loss and then take precautions.

The major cause of losing money in 401(k) is often the fluctuation in the stock market. Stocks, bonds, or mutual funds you invest in may go up or down depending on the market price. This implies that your investments will be at risk when EMH is not functioning fully, resulting in losses during economic downturns/ market corrections. For example, in 2008, 401(k) accounts suffered a lot. However, one has to bear in mind that these losses are often on paper and only crystallize when you dispose of your securities.

The allocation of the funds invested through a 401(k) plan also determines the risk of getting a loss. A portfolio of high-risk instruments such as stocks is generally riskier than one based on bonds and other money market instruments. However, you must invest your 401(k) in different investment classes to reduce the above risks. Understanding how to invest the 401(k) money in consideration of one’s ability to tolerate risks and the period of time one is willing to wait is very important to reduce the number of losses.

Automating Your 401(k) Investments

Letting technology in 401(k) investment is a wise way of retirement savings planning that lets computers and mechanisms handle a routine investment but with effective process integrity. Seeking knowledge of how to best handle the automatic features in a 401(k) plan and improving the investment methods go a long way in enriching retirement plans.

One of the simplest forms of automation applicable to 401(k) investments is payroll 401(k) contributions. It enables a certain amount of your income to be contributed to the 401(k) account each time you are paid, thus making systematic and regular savings possible. Automating contributions also eliminates the need to spend the money saved on something else and the dollar-cost averaging strategy, where a fixed amount is invested at regular intervals, irrespective of the market climate. It can also be used to cut the effects of fluctuating prices in the market and bring cost per share to a lower level in the long run.

Another feature within, and tool of, many 401(k) plans is known as auto-escalation. Auto-escalation means that the contribution rate is raised at a certain frequency, which may be annually, by a certain percentage, say one percent. This way, savings are gradually built up over time without much conscious decision having to be made. By beginning with a small contribution rate and gradually growing it, there are ways to increase retirement savings without feeling too much of a pinch in today’s disposable income.

Another excellent choice for automating your 401(k) investment is target-date funds. Target up funds, which rebalance independently, depending on the certain retirement year. For instance, if you want to retire in 2045, the available target date funds to choose from can have that year as a reference. The fund will initially invest more of its money in stocks to attain growth, though a higher proportion of bonds will be invested nearer the target date. Investment in stocks will, therefore, be larger at the start of the fund than at the end of the period. This automation also helps ensure that the investment strategy is adjusted properly as time comes closer to retirement about your risk tolerance levels.

Auto-Escalation

Auto-increase proposals are also present in 401(k) plans, where your contribution rate is adjusted to increase gradually. This strategy enables you to save more for retirement without altering your lifestyle. It helps you gradually increase your balance and make the best retirement preparations.

Auto-escalation is appealing because it is easy and does not require much interference. Auto-escalation means you do not have to change the contribution rate annually, as the system does for you. Usually, this feature raises your contribution rate by a fixed percentage, for example, 1 percent every year or on a promotion. For instance, it may set your 401(k) contribution to 5% of your salary and then add 1% to the percentage annually, thus auto-escalation. Setting up auto-escalation is one of the best ways to increase your retirement savings without doing much tweaking. This gradual increase does not significantly affect the take-home amount; thus, it barely feels like an improvement. Such slight increments are cumulative and have the effect of significantly boosting your retirement kitty. Getting to know how to invest one’s 401(k) will go a long way in complementing the positives of auto-escalation, as it will make sure that the extra contributions are well invested.

Target Date Funds

An example of such funds is targeting date funds that have gained acceptance for the users of 401k schemes who prefer simplicity in managing retirement schemes. These funds are indexed to change the investment mix at a given date in the future, thus giving an automatic investment service that evolves with time. Knowing the specifics of how target date funds operate and the advantages they afford can assist you in ascertaining the right approach to selecting the best 401(k) investment. Target date funds are established with a particular year for retirement, say five-year intervals (i.e., 20i.e., 2040, 2050). The fund’s investment management is based on the idea of the retirement year, and the closer this year is, the more conservative it is. Initially, target date funds have aggressive investments with more volatile but higher-paying investments such as stocks. In this phase, the fund prepares to liquidate the investments. The retirement date is a target date, so the fund systematically invests more conservatively in bonds or cash, mostly in bonds and cash.

Another advantage of the target date funds is their simplicity and ease of operation. The mutual fund form of organization relieves investors from having to actively manage their portfolio or make sophisticated decisions concerning the diversification of investments. It only means that by selecting a target date fund corresponding to the desired retirement, they can use expertise in managing investments because these are shifted independently over time. This investment approach is suitable for people who wish to have autopilot regarding what they want from their 401(k) investment.

Stay With Your Old Plan

Choosing between keeping money in the old 401(k) plan or transferring it can be one of the most important choices concerning retirement savings. It is crucial to comprehend the differences between remaining consistent with your old plan or rolling over your 401(k) to a new plan or an IRA so your retirement investment can continue expanding efficiently.

Another advantage specific to continuing the old 401(k) plan is the possibility of preserving a choice of investments. Particular 401(k) programs provide peculiar investment options, including institutional funds that cost less in expenses or other particular choices of investments unknown to other programs. Thus, by leaving the money in the old plan, you may invest in these options as long as they respond to the general strategy. Also, if you saw excellent investment options or a good performance history of your previous employer plan, it will benefit you to continue your investment.

Keeping with the old 401(k) may be beneficial to balance one’s portfolio or maintain a tax-deferred growth environment. With 401(k), your investments in a 401(k) product are made without the taxes on earnings being deducted until later, often when one gains from the investment by withdrawing funds. Therefore, despite a shift of your funds to this plan, this tax advantage is well preserved. Leaving your money in the old plan means you do not have to be exposed to a taxable event that you would be subjected to if you withdrew your money or transferred it to another plan.

However, it is also possible for you to remain in your old 401(k) plan and encounter certain issues. The first is rigidity and the inability to control the interface’s behavior and appearance precisely. Restricted choices characterize most previous hirers’ 401(k) schemes and might not allow the plan participants to invest in the latest investment instruments and facilities. Moreover, having several retirement accounts could, over time, be cumbersome, especially in terms of changing, updating, and monitoring the portfolio choice made due to the complexity of the investment plans chosen across the different retirement accounts.

Move Your Savings

Transferring your savings from an old 401(k) plan to a new plan or an IRA is wise when planning for retirement investment. This process is also termed a 401(k) rollover, and it pertains to moving funds for account consolidation or better investment options. Information on the advantages and possible disadvantages of transferring your savings gives you something to consider.

This is one of the main goals of transferring your money, and it consolidates various retirement plans. If you jump from one company to another, you must have multiple old 401(k) accounts. Combining these accounts into a single 401(k) plan or IRA is beneficial because it is easier to monitor the funds, invest correctly, and check assets’ performance aligned with your strategies. This type of structure can also minimize the amount of paperwork and improve the organization on the way.

Another advantage of your savings relocation is the ability to invest in better instruments here. With new 401(k) plans or IRAs that boast a wider choice of products, one can invest in low-cost index funds, ETFs, or even individual securities. In response to this possibility, you can choose new investment strategies that suit your risk profile and your vision for retirement age. This characterization provides flexibility to the portfolio to suit one’s financial requirements.

Cash Out Your Savings

Distributing the funds from 401(k) savings is one of the withdrawal methods that are, from time to time, considered by people when they switch employers or experience urgent financial situations. However, one must be fully aware of the consequences that would come out of this decision, as it is quite a major decision for your post-retirement life. If you decide to cash in on your 401(k) account, you are taking all the money out and terminating the account. It is an efficient way of fixing any difficult financial problems, hence having the following demerits. First, it means a taxable occurrence when one withdraws money from the 401(k). The money you take out is considered similar to your salary, which is charged the normal income tax and, therefore, a large tax can be imposed on the year to be paid. Also, suppose you are under the age of 59 ½ years. In that case, a 10% early withdrawal penalty shall be imposed on the withdrawn amount, further reducing the willingness or money you would possibly be getting from that investment.

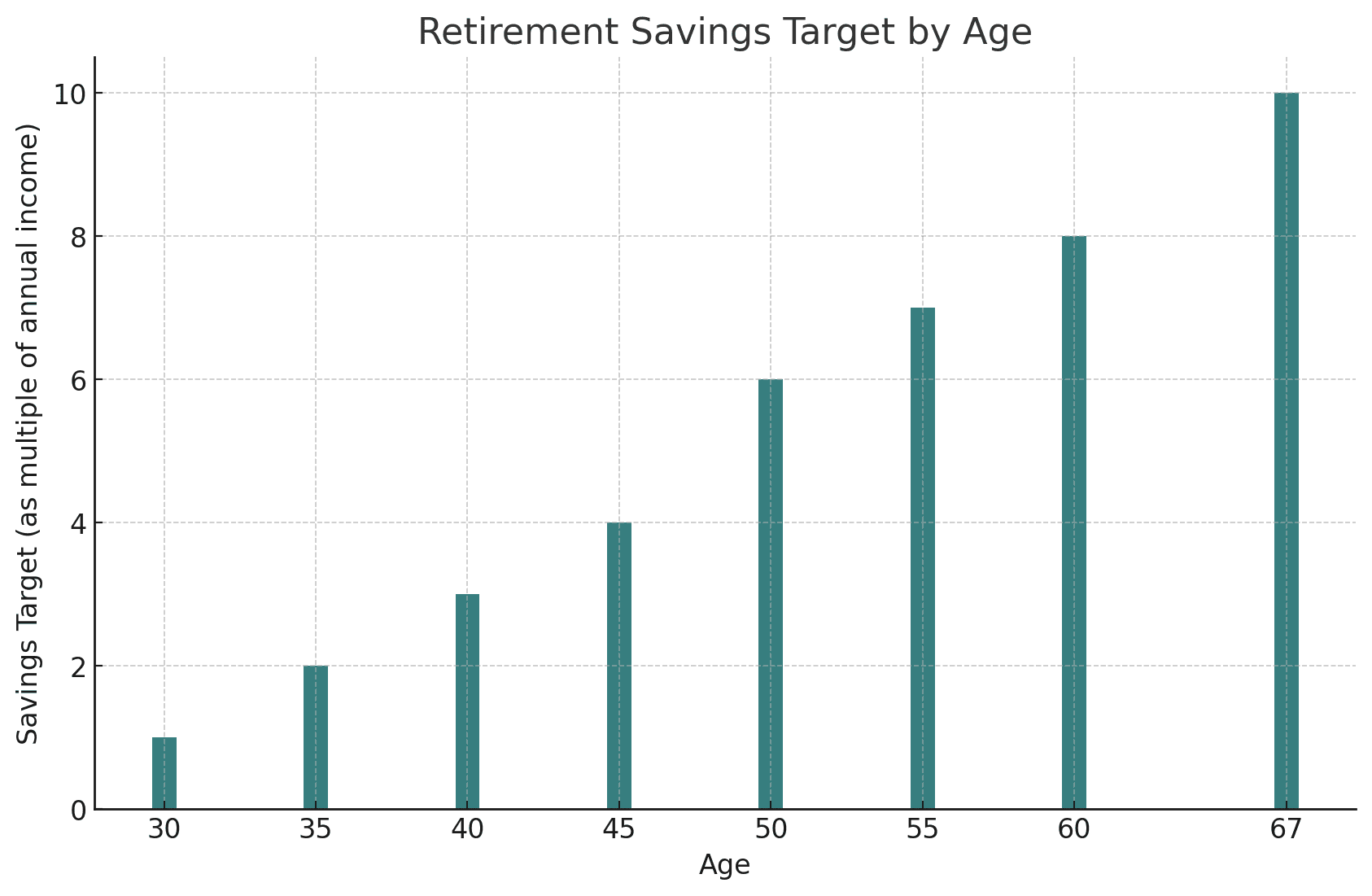

How Much You Should Have Saved For Retirement

Age 35: Building a Strong Foundation The main focus in this stage, by age 35, is to develop a good retirement plan. This is usually the amount most financial advisors suggest should be invested in 401(k) or any other retirement plan by this age; the amount is usually equated to the salary an individual earns within a year; therefore, one should have between one- and two-years’ worth saved for retirement. For example, if one earns $60,000 per year, they should have saved from $60,000 to $120,000.

Age 50: Catch-up Contributions and Strategic Planning At 50, you get what is termed as catch-up contributions for the 401(k), which means you can contribute more than what is stipulated in the law. The catch-up contribution limit that applies to persons at least 50 years of age when the contribution was made is $7,500 for 2024; nonetheless, it is additional to the regular limit of $22,500. Using catch-up contributions can greatly affect your savings level during these essential years. Assessing the investment strategy, you use is also something that you need to consider. As the years to retirement tick down, perhaps reduce the percentage of investments invested in more risky stocks to avoid seeing the pile dwindle in value. However, it is desirable to have a continuation of funds growth; therefore, it is necessary to maintain constant exposure to growth assets.

Age 60: Preparing for Retirement Ideally, by the age of 60, one should have saved 6 to 8 times the amount of their annual salary. Regarding income being $100,000, it is recommended that the amount in retirement accounts be between $ 600,000 and $ 800,000. Such savings should inspire a good life after the working years if one persists in saving and investing. It is during this stage that an individual needs to be more cautious about the preservation of their wealth while at the same time obtaining capital appreciation. Thus, an individual allocated to invest in 401(k) must choose relatively secure options capable of yielding the returns they want to achieve.

Assuming an annual income of $50,000:

| Age | Savings Target |

|---|---|

| 30 | $50,000 |

| 35 | $100,000 |

| 40 | $150,000 |

| 45 | $200,000 |

| 50 | $300,000 |

| 55 | $350,000 |

| 60 | $400,000 |

| 67 | $500,000 |

Conclusion

You can hardly overestimate the importance of getting the most out of your 401(k) investments if you are to retire comfortably. As we covered the peculiarities of managing 401(k), it cannot be denied that special research and wise planning are important to succeed with your retirement. Whether it is the effect of age, diversification ratio, amount to be saved, or automation, each element plays a part in constructing a good retirement portfolio. In managing 401(k) plans, it is best to diversify and invest with the risk-reward proposition depending on time to retirement and goals. Young investors have more years of investment to afford high-risk Books with high stock returns. That is why, over time, diversifying to bonds can help you sustain your capital and, therefore, decrease the risk. This shift in investment is crucial to shield one’s retirement savings plan as one ages. It is, therefore, very important to diversify your investment portfolio as it is one of the keys to a safe Investment. Diversification is the process of investing across different forms of assets, different industries, and different geographic locations to reduce the risks and, hence, increase the chances of getting a stable income on the investments. Diversification avoids high risks because a decline in one sector will not affect the portfolio too much. Learning to invest in 401k, other than stocks, will also help safeguard one’s retirement years by protecting the money from market swings and other economic instabilities.

Responses (0)